Savings Plan

The Conduent Savings Plan is a great way to prepare for the future. Save through payroll deductions, receive tax savings and look ahead to retirement.

Who Is Eligible?

U.S. Conduent associates, including associates classified as part-time, Temporary, or Project Based, are eligible for the Savings Plan.

You are not eligible if you are:

Covered by a collective bargaining agreement that does not provide for your participation in the Savings Plan;

A leased employee;

An independent contractor or consultant; or

A nonresident alien who does not receive U.S. source income

For Associates in Puerto Rico

If you live in Puerto Rico, go to bpas.com for information on your Savings Plan. You may also call the Participant Service Center at 1.866.401.5272.

How Much Can You Contribute?

As a U.S. Conduent associate, you can contribute from 1% to 75% (6% if you are a highly compensated employee) of your eligible pay, up to IRS limits. If you will be age 50 or older in the calendar year, you can make additional catch-up contributions.

IRS limits and definitions for 2025

$23,500 for pre-tax and/or Roth after-tax contributions

$7,500 for pre-tax and/or Roth after-tax catch-up contributions (eligible if you will be age 50 or older in 2025)

If you are a highly compensated employee (HCE), the Savings Plan limits the percentage of eligible compensation you may contribute. Conduent will notify you in April each year if you are an HCE for the current year.

For the 2025 plan year, an HCE is defined as an employee who earned more than $155,000 during 2024. Earnings are calculated using:

Earnings reported in Box 1 of your 2024 W-2

401(k) deferrals

Pre-tax benefits premiums

You can save in one or a combination of the following ways.

Pre-tax 401(k) contributions are deducted from your paycheck before federal income taxes are withheld. You pay taxes on these contributions and earnings when you withdraw the money from the Savings Plan.

Roth after-tax 401(k) contributions are deducted from your paycheck after federal income taxes are withheld. You will not pay taxes again on these contributions or on the earnings if you receive the money as a qualified distribution. A qualified distribution means you have your Roth after-tax account open for at least five years, and you take your distribution after age 59½ or due to death or disability.

You may change, stop, or restart your pre-tax and/or Roth after-tax contributions at any time.

Rollover Contributions

If you have a balance in an existing retirement plan with a prior employer or a rollover IRA, you may roll over that account into your Conduent Savings Plan. Learn what a rollover is and why you should consider rolling over money into your Conduent Savings Plan. To request or print a rollover contribution form, log in to BenefitsWeb.

Conduent Helps You Save

After you complete one year of service, you’re eligible for matching contributions from Conduent. The match is discretionary and will range from 0%–4% based on the company’s financial performance. Conduent does not match catch-up contributions or rollover contributions. Conduent calculates your match on a per-paycheck basis on eligible pre-tax or Roth after-tax contributions that you are making. Conduent credits matching contributions to your account in the quarter following the end of the calendar year. You must be employed on the last day of the year in order to receive the employer match for that year.

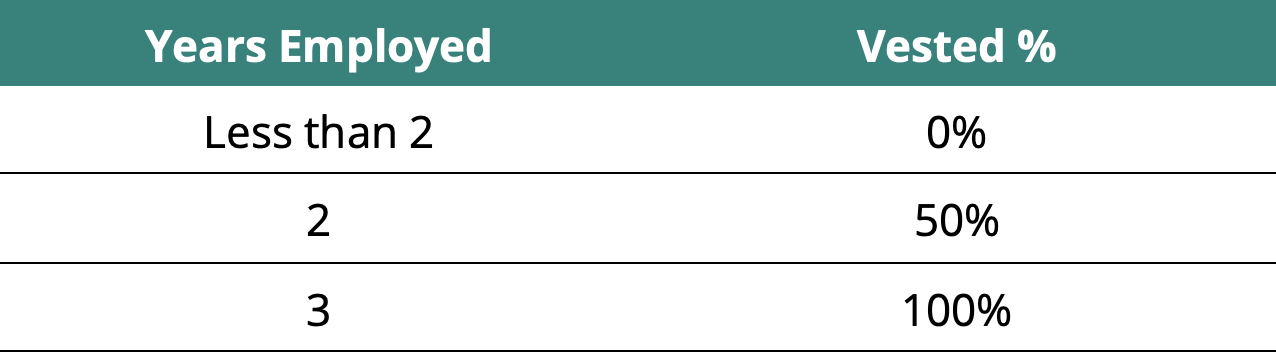

You Vest in Conduent Contributions Over Time

Vesting means gaining ownership. You are always 100% vested in your contributions and rollover contributions. You gain ownership of Conduent matching contributions over time as shown in the chart.

Let’s assume you leave Conduent after working there for two years. In that case, you will be vested in — or own — 100% of your contributions (pre-tax, Roth after-tax, catch-up, and rollover contributions) and 50% of Conduent’s matching contributions. You will forfeit the remaining 50% of Conduent’s matching contributions. If you continue to work at Conduent for three years, you will be 100% vested in your entire account balance.

You will become 100% vested automatically when you reach age 65, in the event of your death, or if you become disabled while employed.

Pick Your Investing Approach

You may invest the money contributed to the Savings Plan using a strategy that fits your investment style. If you do not choose your investments, your contributions will be invested in the Qualified Default Investment Alternative (QDIA).

Want help? Consider Target Date Funds.

With this age-based investment strategy, you pick the fund that is closest to your retirement date. The fund’s investment allocation will automatically adjust over time, becoming more conservative as you get closer to retirement. Learn more about why you might want to consider a Target Date Fund.

Want a more hands-on approach? Choose your own investments.

Pick from a broad range of funds with varying degrees of risk and return.

Review your investments periodically and make changes, as needed. For your long-term retirement security, consider the importance of a well-balanced, diversified investment portfolio, taking into account all your assets, income, and investments.

Prefer additional options? Consider a Self-Directed Account (SDA).

You have the opportunity to open an SDA that allows you to invest in a wide variety of investment options outside of the Savings Plan’s core fund lineup. You will pay $12.50 per quarter to participate in an SDA.

Crack the Code to Investing

Learn the basics. Then, pick the strategy and investing approach in the Savings Plan that's right for you.

Taking Money Out of the Savings Plan

Leaving your money alone to grow is best. However, if you need to access the funds in your account, you may be able to take a loan or an in-service withdrawal (a withdrawal while still working at Conduent). If you leave Conduent or retire, you have several options.

Consider your options carefully as taxes and penalties may apply.

Review or Name Your Beneficiary

When you start participating in the Savings Plan, name one or more beneficiaries — someone to receive your account balance in the event of your death. You can choose anyone to be your beneficiary but keep in mind if you are married, your spouse is automatically your beneficiary unless your spouse gives notarized consent to another beneficiary designation. Review your designation periodically, especially if you have a life status change, such as a marriage or divorce. If you do not name a beneficiary, your account in the Conduent Savings Plan will be paid to your estate.

To update your beneficiary, log in to BenefitsWeb. Select the beneficiaries tab under 401(k) Savings.

To enroll, review or change your elections, log in to BenefitsWeb or call 1.888.471.2271 between 8 a.m. and 8 p.m. Eastern time, Monday through Friday, excluding holidays.